Now that college acceptance letters have started to roll in, students will soon begin receiving financial aid award letters from their prospective colleges, as well. This vital component of the college planning process can be a bit confusing, especially when colleges do not use the Financial Aid Shopping Sheet created by the U.S. government.

This standardized form is meant to help students clearly understand what is being offered and allows them to easily compare award packages from different schools.

Unfortunately, fewer than 2,000 colleges to date have voluntarily adopted this form, which means some students may be unsure of what is actually being offered in terms of financial aid.

First of all, it’s important that students understand that not all financial aid is free money for college. In fact, most financial aid packages include a combination of gift aid and self-help aid. And this is where many students get lost or confused.

They see the total amount being offered, but don’t clearly understand what they are actually taking on in terms of potential debt. Before agreeing to any financial aid package, students must understand the distinct differences between the two types of aid. Here is a brief overview of each, and what students may see as part of their financial aid award packages.

GIFT AID

Gift aid, simply put, is free money for college. Students typically receive gift aid based on financial need, academic achievement, or for other skills and talents. Here are the major types of gift aid commonly offered to students:

Grants

In general, grants are awarded to students based on financial need. This may include Pell Grants and Federal Supplemental Educational Opportunity Grants, as well as grants offered through state and institutional programs. Students must complete the Free Application for Federal Financial Aid (FAFSA) so colleges can determine their eligibility for these awards.

Some colleges may even offer small grants to students who have done well academically, especially during the summer semester, if there are additional funds available. Students who lost a parent as a result of military service in Iraq or Afghanistan after 9/11 may also be eligible for the Iraq and Afghanistan Service Grant, even if their Expected Family Contribution (EFC) is too high for a Pell Grant.

Scholarships

Students can receive scholarships from a variety of sources and for a variety of reasons. The most common scholarships awarded by colleges are for financial need or academic achievement. Students may receive an award based on their SAT or ACT scores, class rank, grade point average (GPA), as well as the ethnic background, or their intended major.

In addition, student athletes at an NCAA Division I or Division II school may receive a scholarship for their particular sport. Those students who have a special talent, such as music or theater, may also receive a scholarship to help offset their costs.

It’s important to note that students can also receive scholarships from state agencies and private providers, such as local businesses and charitable organizations, though these may not be included on the financial aid award letter from their prospective schools.

Students must report any outside scholarships received to their college’s financial aid department, as it will be counted toward the total financial aid allowed and must not exceed the Cost of Attendance (COA).

SELF-HELP AID

Self-help aid is money awarded to students that must be paid back, or requires something in return, such as volunteer hours or a certain number of work hours. This includes the following categories:

Work Study

This need-based financial aid program is offered through colleges and supplemented by the federal government. Funding is limited, so it’s important that students apply early and indicate their interest when completing the FAFSA. If eligible, students may seek or be assigned part-time work either on or off campus.

The hours are typically very flexible and the money is paid directly to the student. Money earned through work-study programs is not counted as income when students apply for FAFSA the following year, therefore it will not lower their financial aid eligibility.

Some schools offer their own work study program unrelated to the federal program and wages earned will count toward student income reported on the FAFSA.

In all cases, it’s important to know that these grants must be earned through work and that the award will not be directly applied to a student’s tuition bill.

Student Loans

Students may be offered federal loans, private loans, or a combination of the two. Unlike gift aid and work-study programs, the money received through loans must be repaid.

In general, federal student loans offer lower interest rates and have more flexible repayment terms for students. There are two federal student loan programs available. The largest, the Federal Direct Student Loan Program (FDLP), includes Direct Subsidized and Direct Unsubsidized Loans, Direct PLUS Loans, and Direct Consolidation Loans. The other, the Federal Perkins Loan Program, is a school-based loan program that is awarded to students who show exceptional financial need.

Eligible students may receive these loans regardless of their credit history, except in the case where a parent or graduate student is requesting a PLUS Loan.

Private student loans, on the other hand, require a good credit score. Most students will also need a cosigner with good credit to obtain a private student loan. It’s important that students review the interest rate, loan fees, Annual Percentage Rate (APR), length of repayment, and total cost of the loan before signing any documents.

Each lender is different, and some may have more favorable terms or offer repayment incentives, so students should compare offers carefully before making a decision.

Private loans should only be used when all other forms of financial aid have been exhausted, and students should only borrow the minimum amount required.

Students may find that their financial aid packages fall short of covering all of their expected expenses, especially if they have a high EFC and do not qualify for need-based assistance.

If there have been changes in their income, a recent hospitalization, or other factors that may have reduced their available college savings, students should contact their college financial aid office and request a review. In some cases, students may be awarded additional financial aid.

For those who still find themselves lacking the necessary funding for college, I suggest looking into other options, such as employer tuition assistance or reimbursement programs, or using a free scholarship search.

If you’re thinking about taking out a private student loan for college, chances are you’ll need a cosigner to get one. Very few students meet the qualifications for securing a loan on their own, so getting your student loans with cosigner may be a necessity. In fact, “more than 90 percent of private student loans for undergraduate students…require a creditworthy cosigner” according to Mark Kantrowitz of Cappex. There are several student loan cosigner requirements to look into.

Table of Contents

A good student loan cosigner cannot only help you secure a student loan, but also obtain a more favorable interest rate. It’s important, however, to understand the risks a cosigner assumes when he or she agrees to help you obtain a loan. He or she will be equally responsible for paying off the debt, even if you don’t finish college.

Should you fail to make payments, your cosigner will be required to not only cover the past due amount, but also any interest fees and other charges that have been assessed. You should only turn to private students loans with a cosigner once you have exhausted all other possible funding sources, such as federal student loans and scholarships. If you do need to pursue a private student loan, you should know who can cosign a student loan and also be aware of the student loan cosigner requirements before asking someone to set up as your cosigner.

What are the Student Loan Cosigner Requirements?

Cosigners for student loans typically need a good credit score, stable income, be in good health and be willing to help you if you are unable to meet your loan payments.

1. Credit History of Cosigner

After the financial and credit crisis of 2008, it became more difficult to qualify for unsecured consumer credit. In the case of private student loans, most borrowers will need a cosigner who has a favorable credit history and a reliable source of income. Your cosigner should have a low debt to income (DTI) ratio, as well as a history of making payments on time.

There are frequently student loan cosigner minimum credit score requirements. Lenders are more likely to approve your loan if your cosigner’s credit score is 720 or higher. If your cosigner has a credit score between 680 and 720, he or she may still be able to help you secure a loan, but the interest rate will probably be higher.

2. Stability

Along with a good credit history, lenders will also look at the stability of your cosigner. This includes job history, as well as the length of time your cosigner has lived in his or her home.

You’ll want to choose someone who has worked for the same company for at least a year, if not longer, and has verifiable income. The longer he or she has lived in the area, and maintained a steady income, the better your chances are of securing a private student loan.

3. Good Health

Believe it or not, the age and health of your cosigner does matter. Maybe not so much to the lender, but it should be something you take into consideration. If you choose a cosigner who is in poor health, or over the age of 65, you may be in for an unpleasant surprise later on.

Why? Some lenders include a clause in your student loan agreement that allows them to demand your loan be paid in full upon the death of your cosigner. Or worse, the lender could place your loan in default, even though you have made all your payments on time.

This can happen automatically, without any notice, and effectively ruin your credit.

4. Relationship to Student Loan Cosigner

You may think that your parents are the only ones who can cosign a loan for you, but that is not the case. Other relatives, including siblings and cousins, as well as a friend or a spouse, may act as your cosigner. Basically, anyone with a good credit history and the willingness to help you could act as your cosigner.

Just remember that this is a binding contract. If you fail to make your payments or default, you run the risk of not only ruining your credit and your cosigner’s, but also destroying your relationship.

It might be a good idea to draft a contract prior to asking someone to act as your cosigner. You could include specific details about how you plan to repay the debt, such as setting up automatic payments, as well as a clause that states you will reimburse any missed payments and/or fees covered over the life of the loan.

It’s not required, but it may give your cosigner some peace of mind. Finally, don’t forget to thank your cosigner for helping you out. It’s a serious commitment to make and one that should not be taken lightly.

With a competitive job market, many people are wondering whether it is the perfect time to attend college. These students are unsure about present and future job prospects along with rising student debt. Also, you may not presently have a job. So you are unsure if you may be eligible for student loans without a job? Learn more about how to receive a student loan without a job.

Can You Get Student Loans Without a Job?

Getting a student loan without a job may be possible when you have a cosigner. A cosigner is someone who may be willing to make your payments. Private lenders will accept this payment arrangement. They are willing take on the financial risk when two people make payments. The recent COVID 19 pandemic has forced many businesses to close and furlough staff. This situation has forced students to worry about paying off their student loan debt. It may also force some students to postpone their college courses until the economy improves.

The U. S. Bureau of Labor Statistics conducted an student unemployment study in January 2020. Unemployed high school graduates made up 3.8 percent of the study. College graduates had a 2.9 unemployment rate during the same month. With these worries, students wonder how they may pay for their college expenses. Student loans without a job could fill in the gaps or pay the entire costs. Students may seek a loan from a private lender. You may also be eligible for federal aid if you qualify. Private loan lenders may offer student loans even if you’re unemployed or if you have bad credit history. Financial aid may be available to those who qualify.

How Do I Qualify for Student Loans Without a Job?

One way to qualify is to have a cosigner. Private lenders take into consideration a person’s employment history and credit history. This information allows lenders to figure out the amount of the loan. A cosigner is anyone who meets the eligibility criteria for the student loans without a job. The cosigner may be your parents, grandparents, or another family member. It may also be a spouse or family friend. The cosigner typically have to meet the following criteria:

Income minimum limits and debt to income ratios may vary between lenders. You may need a cosigner if you don’t have a job. Ensure that the cosigner is someone that you trust.

Can You Get Federal Student Loans and Private Student Loans Without a Job?

Both private and federal aid lenders may provide student loans to unemployed students. You should double check if you meet the eligibility requirements of each lender.

What Federal Student Loans May You Receive Without a Job?

U.S. Department of Education will not review your credit report. The organization will also not check income history. They provide Stafford loans based on financial need. You also typically don’t need a cosigner. The only exception to this rule is if you plan to take out a Direct Plus loan with poor or no credit history. In these instances, you may need to have an endorser, which is similar to a cosigner.

Types of federal student loans that you may be eligible for if you don’t have a job include:

Direct Subsidized Loans: A federal student loan for undergraduate students. You may have to show financial need. The federal government will pay the fixed interest rate for the life of the loan.

Direct Unsubsidized Loans: A federal student loan for undergraduate and graduate students. You do not need to prove financial need. This federal student loan usually has fixed interest rates for the life of the loan.

Federal student loans typically have lower interest rates. This option also provides more variable payment options than private loans. You need to fill out a free application for federal student aid (FAFSA). Then you may send it to the eligible financial institution. The eligible financial institution may determine the amount of the federal loans.

What Private Student Loans Are Offered to Unemployed Students?

Private student loans may be available for unemployed students. You may need to have a cosigner to receive the loan. Citizens Bank and Sallie Mae may provide student loans. You may also seek out financial loans from a credit union. Private lenders may check your credit history and employment history for loan eligibility.

Other private lenders may check your future income potential instead of doing a credit check. This factor occurs when you don’t have a credit history or a co signor. Lenders understand that you may find employment after college. In this instance, you may be able to obtain one and submit a loan application.

How Do I Repay Student Loans Without a Job?

You may have to repay the personal loan using the funds from a savings account. The cosigner may also make monthly payments for you during your unemployment. Then you can take over the remaining loan amount or repay the cosigner. You could ask for forbearance or deferment for federal student loans. Forbearance may suspend your federal loan payments. The interest will still accrue on the loan as you will need to pay it later. Deferred federal loans will not accrue interest.

You may also qualify for loan forgiveness programs or an income driven repayment plan for federal loans. There might be less private student loan repayment options for unemployed students. Some student loan lenders may offer unemployment protection or economic hardship forbearance. You may check with specific loan servicers and student loan options. They may inform you about the length of their repayment term’s grace period. Also, don’t forget to check the repayment terms in the loan agreement which has the contracted interest rate.

Loan Forgiveness Programs: Loan forgiveness programs may forgive the remaining loan amount. You may have to make a certain number of previous payments to qualify. Private loan providers typically do not offer loan forgiveness programs. Federal loan forgiveness programs include the Public Service Loan Forgiveness Program.

Income driven Repayment Plan: An affordable payment program based on your income and family size. The PAYE plan applies to federal loans. Sallie Mae offers a $25 payment option while you’re in school and during the grace period.

Unemployment Protection/Economic Hardship Forbearance Programs: Some private lenders may offer deferment or forbearance programs. They’re available if you may experience unemployment or economic hardships. The Citizen’s Bank Student Loan offers deferment options. They may defer interest and payments for 6 months after graduation.

What Other Options May Help Pay for College?

You may try to pursue other financial aid options. Grants and scholarships typically do not need you to pay back the funds if you graduate. Yet, certain grants, such as a Pell Grant, may need repayment if you drop out of college. Other options may include:

Waiting to go to college until after finding a job

Placing the extra money into a savings bank account until you have enough for college

Obtaining a part time job, either online or at a brick and mortar establishment

The pandemic has caused increased economic uncertainty on a global scale. Many students are reconsidering their career options right now. You may select the loan options that best fit your current job goals. Then you could receive the desired degree at a great college.

Get Informed, Then Get Matched To Online Schools Using Our Degree Finder!

Table of Contents

PICKING A STUDENT LOAN REPAYMENT PLAN

When dealing with federal student loans, you’re presented with a menu of eight distinct repayment possibilities. Familiarizing yourself with these options is crucial in order to pinpoint the one that aligns most favorably with your financial circumstances. To accomplish this, it’s imperative to evaluate your individual requirements, encompassing an understanding of both your monthly budget and the time frame available for settling your loan.

An online tool at your disposal for aiding this decision-making process is the Repayment Estimator offered by the Department of Education. By inputting specifics such as your loan balances, interest rates, tax filing status, income, and family size, this tool serves to generate a comprehensive array of potential strategies:

Which repayment plans you are eligible for

The amount of your first and last monthly payments

Total amount paid

Any projected loan forgiveness

How long you have to repay your student debt

Since there are different plans and grace periods, it is crucial to get to know the features of each choice. Often, a student loan servicer can work with you, but it is a good idea to go into a meeting prepared. For quick reference, the main types of student loan repayment plans are as follows. Before you start, these differ from the ways you’d pay back a private loan, which we discuss further on in the article.

Standard Plan

Extended Plan

Graduated Plan

Income-Driven Plans

Income-Sensitive Plan

STANDARD REPAYMENT PLANS (SRP)

The Standard Repayment Plans (SRPs) serve as the default payment arrangement for both Federal Direct Loans and Federal Family Education Loans (FFEL). These plans grant you the opportunity to clear your loan within a span of 10 years, during which you’ll be making fixed monthly payments. The exact amount of these payments is contingent upon your loan balance and is meticulously calculated to ensure complete repayment within the stipulated decade. However, it’s important to note that you might need to fulfill a minimum monthly payment of at least $50 throughout the entirety of your loan’s lifespan.

An appealing facet of the Standard Repayment Plan is its inherent flexibility. In the event of encountering financial hardships, you have the liberty to transition to an alternative plan. Conversely, if all unfolds as anticipated, you can bid adieu to student debt after the span of 10 years, subsequently diverting your focus toward other financial aspirations.

Another point to consider pertains to the matter of interest charges. When juxtaposed with the Income-Based Repayment Plans (which we shall delve into shortly), the Standard Repayment Plan tends to entail lower interest fees. This divergence can be attributed to the elongated duration of Income-Based Repayment Plans, which could potentially lead to higher accrued interest. Nonetheless, it’s worth noting that this plan’s monthly payments might surpass those associated with certain alternative plans.

INCOME-DRIVEN REPAYMENT PLANS (IDR)

For those grappling with student loan debt, income-driven repayment (IDR) plans can serve as a valuable tool. These plans achieve this by reducing your monthly payment obligations, offering immediate relief to your cash flow. Nevertheless, it’s essential to recognize that over the long haul, you might face implications like taxable income on forgiven loans and elevated interest fees.

Borrowers who qualify have access to four distinct income-driven repayment plans, designed to assist individuals who find it challenging to meet their payment obligations on their current income. In the overview provided below, the significance of your disposable income (discretionary income) becomes apparent when considering these options.

1. REVISED PAY AS YOU EARN REPAYMENT PLAN (REPAYE)

Under this plan, your monthly payments typically amount to 10 percent of your discretionary income, divided by 12. Any remaining balance is eligible for forgiveness after 20 or 25 years.

2. PAY AS YOU EARN REPAYMENT PLAN (PAYE)

Monthly payments, within the PAYE plan, are typically equivalent to 10 percent of your discretionary income, divided by 12. Any outstanding balance becomes eligible for forgiveness after 20 years.

3. INCOME-BASED REPAYMENT PLAN (IBR)

Within the Income-Based Repayment Plan, monthly payments usually correspond to 15 percent of your discretionary income, divided by 12. However, if you’re a new borrower, the payment percentage is lowered to 10 percent. Any remaining balance is subject to forgiveness after 20 or 25 years.

4. INCOME-CONTINGENT REPAYMENT PLAN (ICR)

This plan entails monthly payments equal to 20 percent of your discretionary income, divided by 12. Alternatively, it can be the amount you would pay under a fixed 12-year repayment plan (longer than the 10-year SRP). Any remaining balance becomes eligible for forgiveness after 25 years.

EXTENDED REPAYMENT PLAN (ERP)

The Extended Repayment Plan presents you with the option to spread out your loan repayment over a more extended timeframe compared to the Standard and Income-driven plans. In contrast to the 10-year term of the SRP, you have the ability to make payments over a span of up to 25 years. During this period, your payments can either remain fixed or follow a graduated pattern. Generally, this translates to more manageable monthly payments compared to what the Standard and Graduate Repayment Plans demand. Nonetheless, if your objective is to swiftly eliminate your student debt in order to allocate funds for purposes such as purchasing a house, retirement, travel, or other aspirations, this plan might not align with your goals.

GRADUATED REPAYMENT PLAN (GRP)

The Graduated Repayment Plan initiates your repayment journey with lower initial payments that increment every two years. In essence, you remain on a 10-year track (or a 30-year track for consolidated loans), but your monthly payments commence at a lower level and progressively rise. This payment structure assumes that as you advance in your career, you’ll be in a position to make more substantial contributions toward your loan.

UNDERSTANDING LOAN REPAYMENT

Your student loan billing is managed by your loan servicer, and each servicer follows its own payment procedure. It’s your responsibility to directly submit payments to your servicer; however, they often offer assistance if needed. In case you’re unsure about your servicer’s identity, you can verify it by checking your account on My Federal Student Aid.

How much will your payment be? Typically made on a monthly basis, your payment hinges on four key factors:

The specific type of loan you obtained

The total amount you borrowed

The repayment plan you’ve selected

The interest rate associated with your loan

WHAT IS A GRACE PERIOD ?

The time lapse after graduation and before you start making payments is a “grace period”. Usually it is a set time frame which gives you the space to settle your finances and select your repayment plan.

No grace period – PLUS Loans (possible eligibility for deferment) 6-month grace period – Direct Subsidized Loans, Direct Unsubsidized Loans, Subsidized Federal Stafford Loans, and Unsubsidized Federal Stafford Loans 9-month grace period – Federal Perkins Loans Up to 3-year extension – Military service members

Caveat: While it may sound great to have this breathing room, interest will mount up if you have unsubsidized loans. It’s the same when you don’t pay a credit card balance on time.

In contrast, Perkins loans, direct subsidized loans, and subsidized Stafford loans don’t accrue interest during the grace period. You can, however, use your grace period to make interest payments. If this is easy for you to do, it’ll put you one step ahead when your grace period is up.

DEFERMENT OR FORBEARANCE ON FEDERAL STUDENT LOANS

Do you need to postpone your payments? In some cases, one may be eligible to receive a deferment or forbearance. These are temporary pauses which allow you to stop making payments. Or, reduce your monthly payment amount for a specified period.

For instance, there’s a provision in the Department of Education Appropriations Act, 2019 which allows cancer patients to get deferments while they are in treatment. Part-time students, military persons and others may also be eligible for a deferment.

One thing to remember is that with a deferment, you may not be responsible for paying the interest your loan amasses. This applies only to specific types of loans. During a forbearance though, you are responsible for paying the interest that accrues on all types of federal student loans.

LOAN CONSOLIDATION

Do you have many federal student loans? You may be able to merge them into one loan with a fixed interest rate. The amount of the loan depends on the average of all the joined interest rates and there is no cost to you. To do so, you need to file a Federal Direct Consolidation Loan Application and Promissory Note. Overall, this may simplify your repayment process.

PUBLIC SERVICE LOAN FORGIVENESS (PSLF)

The Public Service Loan Forgiveness Program is a federal program. It forgives the remaining balance on Direct Loans for eligible student loan debt holders. How do you qualify for public service loan forgiveness? To be eligible for PSLF, you’ll need to meet several criteria:

Where you work matters. Qualifying employers include the government or not-for-profit organizations.

You must first enroll in a qualifying repayment plan. Examples include REPAYE, PAYE, IBR, ICR and SRPs.

You need to be a full-time employee. This means more than 30 hours per week.

Under one of these plans, you’ll have to make 120 qualifying monthly payments.

UNDERSTANDING FEDERAL INCOME-DRIVEN REPAYMENT PLANS

Are your federal student loan payments high compared to your income? If so, you may want to repay your loans under an income-driven repayment plan. Most federal student loans are eligible for at least one (of the four) income-driven repayment plans.

If your income is low enough, your payment could be all of $0 per month. Remember though, you’ll need to make calculations using your discretionary income as a guide. To calculate your discretionary income, find the difference between your adjusted gross income and 150 percent of the annual poverty line for a family of your size and in your state.

You may also want to familiarize yourself with the different repayment periods and payments. The table below is an overview of this information.

Income-driven Plan Name

Term Length

Monthly Payment Cap

Description

Income-based repayment (IBR)

20 years if you’re a new borrower on or after July 1, 2014 OR 25 yearns if you’re not a new borrower After July 1, 2014

10% of discretionary income (for new borrowers) on or after July 1,2014 but never more than the 10-year Standard Repayment Plan amount OR 15% of discretionary income if you’re not a new borrower on/or after July 1,2014

Low monthly payments

Loans eligible for forgiveness after repayment period

Possibility of higher interest fees

If your loans are forgiven, the balance may be taxable

Income-contingent repayment

12 years

The lesser of either 20% of your discretionary income OR what you would pay on a repayment plan with a fixed payment over the course of 12 years, adjusted according to your income

No income eligibility requirement may make it easier to qualify

You may be eligible for loan forgiveness

Parents with PARENT PLUS Loans can qualify once they consolidate their loans into a Direct Loan

Highest potential payment amount of all 4 plans

If your loans are forgiven, the balance may be taxable

Pay as you Earn

20 years

10% of discretionary income

Lowest payment amount for eligible borrowers

Loans eligible for forgiveness after repayment term

Only new borrowers can qualify

If your loans are forgiven, the balance may be taxable n qualify

Revised Pay as you Earn (REPAYE)

20 years if the loans are for undergraduate study OR 25 years if the loans are for professional or graduate study

10% of discretionary income

Lowest payment amount for eligible borrowers

Loan forgiveness terms depend on whether you’re an undergraduate or graduate student

Monthly payments factor in your spouse’s income regardless of filing status

If your loans are forgiven, the balance may be taxable

APPLYING FOR INCOME-DRIVEN REPAYMENT

To apply for one of the Income-driven Repayment Plans, there are some easy steps to follow. You won’t need an application fee, but the process requires you to complete it in one session. If you’re nervous about filling out official forms, you can download a PDF version of the Request and do it manually. Otherwise, here’s how to prepare.

Create an FSA ID (or have your ID number handy)

If you are married, make sure you have your spouse’s SSN and information

Have your personal information and income figures handy

Each year you’ll need to recertify, in order to remain eligible for the lowest possible monthly payment amount.

BASIC FEDERAL STUDENT LOAN REPAYMENT PLANS

Basic Federal Student Loan Repayment Plans often balance a monthly payment you can afford today and a lesser total amount overall than income-driven plans. That said, an IDR may lower your payments today even though in the long run, you may be paying more.

Basic Repayment Plan Name

Term Length

Description

Standard Repayment

10 years

Fixed Monthly Costs

Graduated Repayment

10 or 30 years for consolidated loans

Monthly payment starts out low and gets higher over time

Extended Repayment

25 years

Your payments are either fixed or graduated for the term of the loan

PRIVATE STUDENT LOAN REPAYMENT OPTIONS

Private Student Loans do not qualify for federal income-driven repayment plans. Or forgiveness programs. Yes, a debt is a debt, but Federal Student Loans begin with the U.S. Department of Education. They also come with standard benefits and protections.

The reason for this is that to get a private student loan, you’ll usually deal with a bank. Or, you’ll borrow from a private financial institution. In general, neither comes with either income-based repayment plans or forgiveness options.

Also, because these institutions don’t have to offer financial assistance to student borrowers, there aren’t as many ways to repay the loan. This limits the ways you can repay your loan, although may have a few options if you start to struggle.

To help you better grasp how to potentially lower your private student loan payments, check out some suggestions below. These may give you some food for thought on how to better manage your monthly payments.

LOWER YOUR PAYMENTS YOURSELF

If you are up for giving it the ‘old college try’, setting a budget that covers your needs rather than wants is a good place to start. Some loan lenders also suggest that you make auto-debit payments which may lower your interest rate. This is useful if you can count on your income (and can generate more money). Not so good if you think you might be hit with overdraft fees.

LOAN REFINANCING

You do need to go through hoops (credit scores for e.g.) set by your financial institution. Yet refinancing student loans may help you manage any flux in your budget. This is where you’ll have to shop around for lenders to see what terms they offer – 5, 7,10, 15 and 20 are common. Some also allow you to merge private and student loans. As such, you may be able to find a lower interest rate, decrease your monthly payment, or both.

LENDER-SPECIFIC REPAYMENT PLANS

Some lenders may offer Repayment Assistance Options to help students manage their loan repayments. Some of these are similar to federal loans, only you’ll have to qualify with a Lender such as Discover.

Deferment – A temporary postponement of payments

Forbearance – postpones your loan payments for up to 12 months during the entire term of your loan, though there are stipulations

Hardship – A temporary reduction of interest rates for up to 12 months, subject to stipulations

Early Repayment Assistance Program – A 3-month postponement of payments

Payment Extension –Allows students to bring their loan current by making 3 minimum monthly payments (or the equivalent amount of 3 minimum monthly payments) within a 90-day period

Reduced Payment – The Minimum Monthly Payment is reduced, subject to a $50.00 minimum, for an initial period of six months.

5 WAYS YOU COULD PAY OFF STUDENT LOANS FASTER

If the prolonged duration of paying off your debt is causing frustration rather than financial strain, there are methods to expedite your journey towards repaying student loans. To initiate this process, acquaint yourself with your projected payoff date, and then strive to bring it closer. Do any of these alternatives seem like opportunities to achieve this objective?

1. MAKE ADDITIONAL PAYMENTS ON YOUR STUDENT LOAN

While the allure of discretionary spending is ever-present, consider redirecting windfalls such as overtime pay, commissions, or tax refunds toward supplementary or lump-sum payments on your loan. Remember, every bit contributes to achieving the goal.

2. EXCEED THE MINIMUM PAYMENT

Should you find yourself with extra funds, contemplate making payments exceeding the minimum requirement either weekly or monthly. This approach provides you with the flexibility to decide how much you wish to contribute beyond the minimum. Alternatively, set up automatic payments slightly above the minimum. Even forgoing the cost of five weekly coffees accumulates over time.

3. EXPLORE LOAN FORGIVENESS OPTIONS

For those embarking on careers in fields like teaching or public service, as previously discussed, loan forgiveness might be attainable. Certain states also provide Loan Repayment Assistance Programs (LRAPs). Naturally, eligibility criteria apply, but this avenue presents an opportunity to channel funds toward settling federal (and occasionally private) student loans.

4.UTILIZE TAX DEDUCTIONS

Ensure that you maximize any applicable tax credits and deductions. If you’re in the process of repaying student loans, you might qualify for the student loan interest deduction on your federal taxes. Assuming you receive a substantial tax refund, adhere to your plan while considering strategies 1 and 2.

5. REFINANCE YOUR STUDENT LOANS

Refinancing stands as a mechanism to expedite debt elimination while securing lower interest rates and monthly payments. To initiate this process, compare various refinance terms to identify the alignment with your goals. Notably, refinancing can alter your monthly payment structure. Therefore, verify that the revised payments are sustainable. If your financial situation is precarious, this step might exacerbate issues. However, if you possess solid credit and income stability, conducting research and exploring different options could prove to be a viable approach.

Federal loans for students offer you the chance to borrow funds for college that you must repay with interest. Often, these federal loans offer a lower interest rate and more flexible repayment terms than private student loans.

Learn all about what types of federal student loans are available to find the best option for you and don’t forget to discover grants and scholarships to help you earn free money for college.

In 2022-23, 85% of first-time, full-time degree / certificate-seeking undergraduate students were awarded financial aid. Overall, 72.3%of all undergraduates received some type of financial aid.

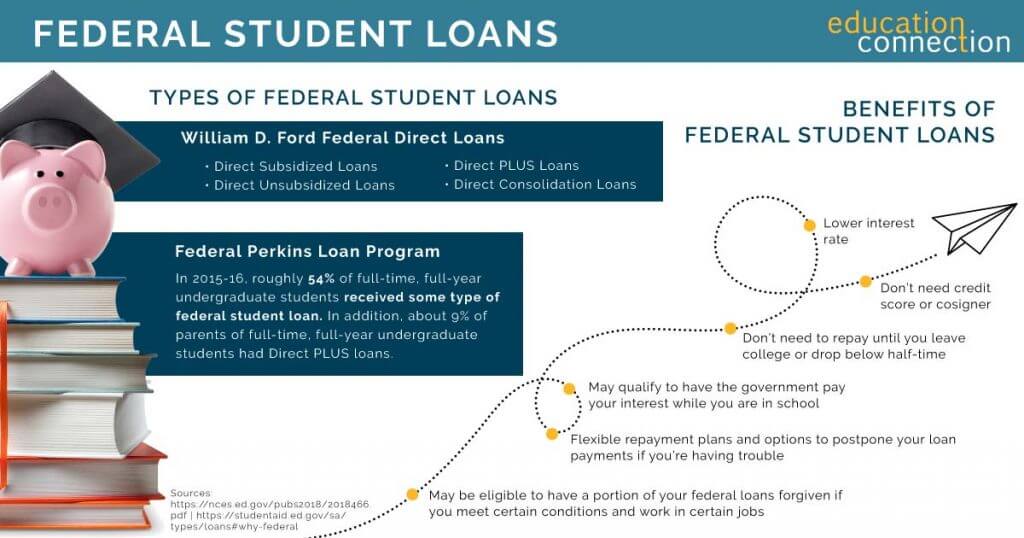

TYPES OF FEDERAL STUDENT LOANS

There are two main types of federal student loans:

William D. Ford Federal Direct Loans

Federal Perkins Loan Program

These loans have unique requirements, interest rates, and maximum awards per year, which are explained below.

WILLIAM D. FORD FEDERAL DIRECT LOANS

This is the largest federal student loan program where the U.S. Department of Education is the lender. These loans include:

Direct Subsidized Loans

Direct Unsubsidized Loans

Direct PLUS Loans

Direct Consolidation Loans

Check out the table below to learn about the differences between these loans.

FEDERAL PERKINS LOAN PROGRAM

As opposed to direct loans, which have the Department of Education as the lender, the Perkins loans are school-based loans, which means that the individual school is the lender.

These loans are offered to undergraduate and graduate students with exceptional financial need. In addition, the amount awarded depends on the amount of funds available at a particular school.

Often, the students with the greatest financial need are awarded Federal Perkins Loans.

TYPES OF FEDERAL STUDENT LOANS

Federal Loan

College Degree Level

Federal Student Loan Program Details

Interest Rate (First Disbursed on or After July 1, 2018 and Before July 1, 2019)

Maximum Annual Award

Direct Subsidized Loan

Undergraduate

For those with financial need

5.05%

$5,500 (depending on grade level and dependency status)

Direct Unsubsidized Loan

Undergraduate, graduate, and professional degree students

Financial need is not required

5.05% (6.6% for graduate or professional)

$20,550 (depending on grade level and dependency status)

Direct PLUS Loan

Parents of dependent undergraduate students; and for graduate or professional degree students

Financial need is not required; borrower must not have adverse credit

7.6%

Maximum amount is cost of attendance minus any other financial aid you receive

Federal Perkins Loan

Undergraduate, graduate, and professional degree students

Eligibility depends on financial need and availability of funds at your school

5.0%

$5,500 for undergraduate students; $8,000 for graduate and professional students

PERCENTAGE OF GRADUATE STUDENTS WHO RECEIVE FINANCIAL AID

71.6% of all graduate students received some type of financial aid, including 44.2% of graduate students who took out some type of loan.

HOW TO APPLY FOR FEDERAL STUDENT LOANS

In order to apply for federal student loans, you must complete and submit a Free Application for Federal Student Aid (FAFSA). Based on these results, your college or career school will send you a financial aid letter, which may or may not include an offer of federal student loans.

This offer includes instructions on how to accept all or part of the loan. However, before you receive your loan funds, you will have to complete two steps:

Complete entrance counseling to ensure that you understand your obligation to repay the loan

Sign a Master Promissory Note (MPN), agreeing to the terms of the loan

As some students may not receive federal student loans as an option after completing the FAFSA, don’t forget about private student loans. While each lender and type of loan have different requirements than federal loans, private loans are available to all students.

BENEFITS OF FEDERAL STUDENT LOANS

Some of the benefits of federal student loans include:

Interest rate on federal loans is usually lower than private student loans

You don’t need a credit check or cosigner for most federal loans

You don’t need to begin repaying your federal loans until you leave college or drop below half-time

If you demonstrate financial need, you may qualify to have the government pay your interest while you are in school

Many federal student loans offer flexible repayment plans and options to postpone your loan payments if you’re having trouble

You may be eligible to have a portion of your federal loans forgiven if you meet certain conditions and work in certain jobs

FAFSA Application Deadline

Normally, online FAFSA applications must be submitted by midnight Central Time on June 30 of a given year. For instance, the 2023-2024 FAFSA deadline is midnight Central Time, June 30, 2025.

FEDERAL STUDENT LOANS – HOW MUCH SHOULD YOU BORROW?

Whether you’re taking out a private student loan or a federal loan, it’s important to consider the legal obligation you have to pay back then loans, so responsible borrowing is key.

Some of the things to consider when borrowing money for college:

Understand your total amount of loans and how this will affect your future finances

Research starting salaries in your field

Understand the terms of your loan

Make payments on time

Often there are flexible repayment terms for both federal loans and private student loans. This includes options such as, grace period, interest-only payments while in school, and interest rate reductions for automatic debit.

Looking for private student loans? Check out some of your options here!

Percentage of Students Stressed about paying for college

According to a 2017 study by The Princeton Review, 98% of college applicants and their parents said financial aid would be necessary to pay for college. Plus, 65% said financial aid was extremely necessary.

OTHER TYPES OF FINANCIAL AID

As the price of college tuition continues to rise understanding the types of financial aid and finding the right combination of financial aid to pay for your degree is just as important as finding the perfect program for you.

Luckily, there are plenty of other options of financial aid for you to choose from, including:

All of these options mean that you don’t have to worry if you need to supplement your federal student loan offer. Discover some private student loans to find the perfect one for you.

FIND THE FINANCIAL AID PACKAGE AND FEDERAL STUDENT LOAN THAT’S PERFECT FOR YOU

Finding the right mix of financial aid is one of the key aspects of earning your degree. That’s why it’s important to consider all of your options and be sure to do your research.

A good starting point is talking to your counselor or the financial aid office at your school, both of which should have specific details for you to explore.